Most gun collectors spend decades building a collection — researching, upgrading, documenting, and refining. But very few spend time planning what happens after they are no longer here to manage it.

That gap can create confusion, unnecessary tax questions, and real problems for the people left behind. This guide walks through the practical, legal, and tax considerations every collector should think through before the collection becomes someone else’s responsibility.

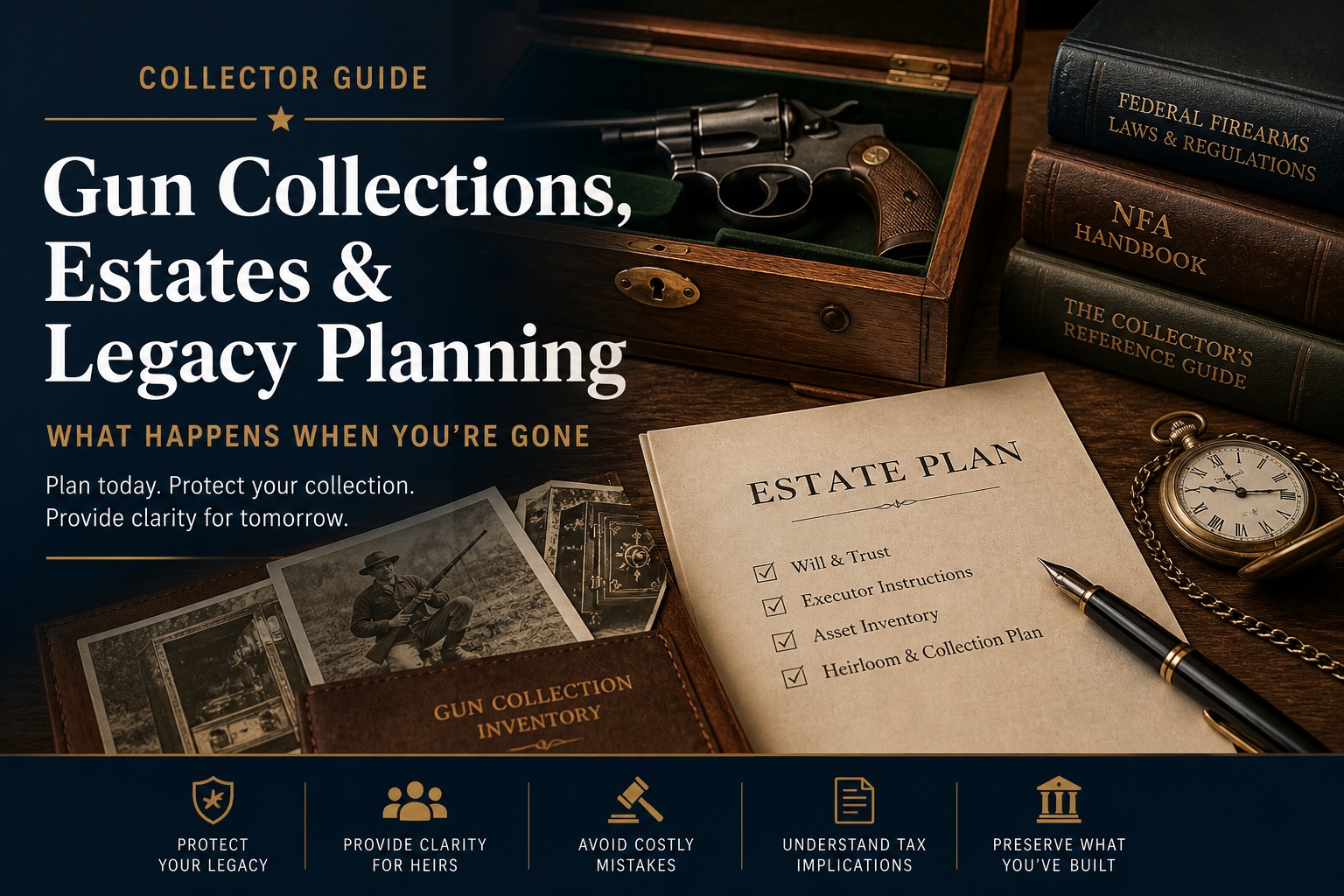

A collection without a plan becomes someone else’s problem.

The Reality Most Collectors Avoid

At some point, one of three things usually happens:

- You sell the collection yourself.

- Your family liquidates it.

- It passes through your estate.

The outcome depends on planning — not luck. A well-documented collection gives your family options. A poorly documented collection puts them at a disadvantage before the first phone call is made.

Step-Up in Basis

When a collector passes away, the cost basis of the collection may receive a step-up to fair market value at the date of death. For many families, this can be the single most important tax issue connected to a collection.

Simple Example

Assume a collector paid $50,000 for a collection that is worth $150,000 at death. If the heirs receive a stepped-up basis to fair market value, that $100,000 of appreciation may not create income tax if the collection is sold soon after death for roughly that value.

That is why a collector should be careful before liquidating everything late in life just to “make it easier.†Sometimes selling during life makes sense. Sometimes retaining the collection, documenting it well, and leaving clear instructions makes more sense.

Sell Now or Leave It to the Estate?

Option 1: Sell during lifetime

Selling during life gives you control. You know the collection, you know what matters, and you can decide what deserves to be sold, kept, or gifted.

The downside is that a profitable sale may create income tax consequences. Depending on the facts, it may also affect taxation of Social Security benefits or Medicare premium calculations.

Option 2: Leave it to heirs

Leaving the collection to heirs may produce better income tax results because of basis adjustment at death. But heirs may not understand the collection, may not know who to call, and may accept dealer pricing simply to get the matter behind them.

The right answer is not the same for every collector. The right answer depends on value, records, family interest, health, state law, and whether your spouse or heirs can realistically manage the process.

The Hidden Risk: Poor Records

If your heirs do not know what you paid, what it is worth, or what makes it collectible, they are at a disadvantage immediately.

Minimum records every collector should keep

- Make, model, and serial number.

- Purchase date and purchase price.

- Estimated current fair market value.

- Condition notes, originality notes, and provenance.

- Photographs stored somewhere separate from the firearm.

- Copies of receipts, letters, auction listings, and appraisals.

Good records are not just for taxes. They help your family avoid selling a high-value piece as if it were an ordinary shooter.

Trusts, Wills, and Simple Instructions

Some collectors assume a trust is always the answer. It may be useful in the right situation, especially with a large collection, multiple heirs, NFA items, or very specific instructions.

But many collectors do not need to overcomplicate the matter. A simple will, a clean inventory, written instructions, and a short list of trusted contacts may accomplish more than an elaborate plan nobody understands.

Legal Transfer Considerations

Heirs can generally inherit firearms, but transfers still need to comply with applicable federal, state, and local laws. State rules vary, and certain firearms may require special handling.

NFA items require additional planning and paperwork. If your collection includes silencers, short-barreled rifles, machine guns, or other regulated items, do not leave your heirs guessing.

The Smart Collector’s Plan

The best approach is usually practical, not complicated:

- Keep collecting within reason.

- Maintain clean records.

- Downsize gradually if that makes sense.

- Tell your spouse or executor where the records are.

- Leave names of trusted dealers, auction houses, or knowledgeable collectors.

- Review the plan every few years.

The Conversation Most Avoid

You should talk to your spouse, children, or executor about what the collection is worth, what should happen to it, and who should be called if you are no longer available to answer questions.

That conversation may feel awkward, but it is far better than leaving family members alone with a safe full of guns, no values, no instructions, and no idea what matters.

Collector Guide Series

This article completes a practical three-part collector planning series:

- Guns, Taxes & Terminologies

- When the Time Comes to Downsize

- Gun Collections, Estates & Legacy Planning

Collector Takeaway

A gun collection is more than a list of objects. It represents years of decisions, stories, research, and personal judgment. A good plan protects that work and gives your family a better chance of preserving value when you are no longer there to guide them.

From My Bench

If you are organizing your own records, storage, or work area, I keep a curated list of tools, books, cleaning gear, and bench items that fit the way I work.

Browse My Gear ListAs an Amazon Associate I earn from qualifying purchases. I only link to products, books, tools, and accessories that fit the editorial purpose of Gun Collectors Club.

About Greg Cook

Greg Cook writes about firearms collecting, personal history, and the stories behind interesting guns. His Army MOS was 76Y, Unit Armorer, and he brings that practical background to his collector articles.