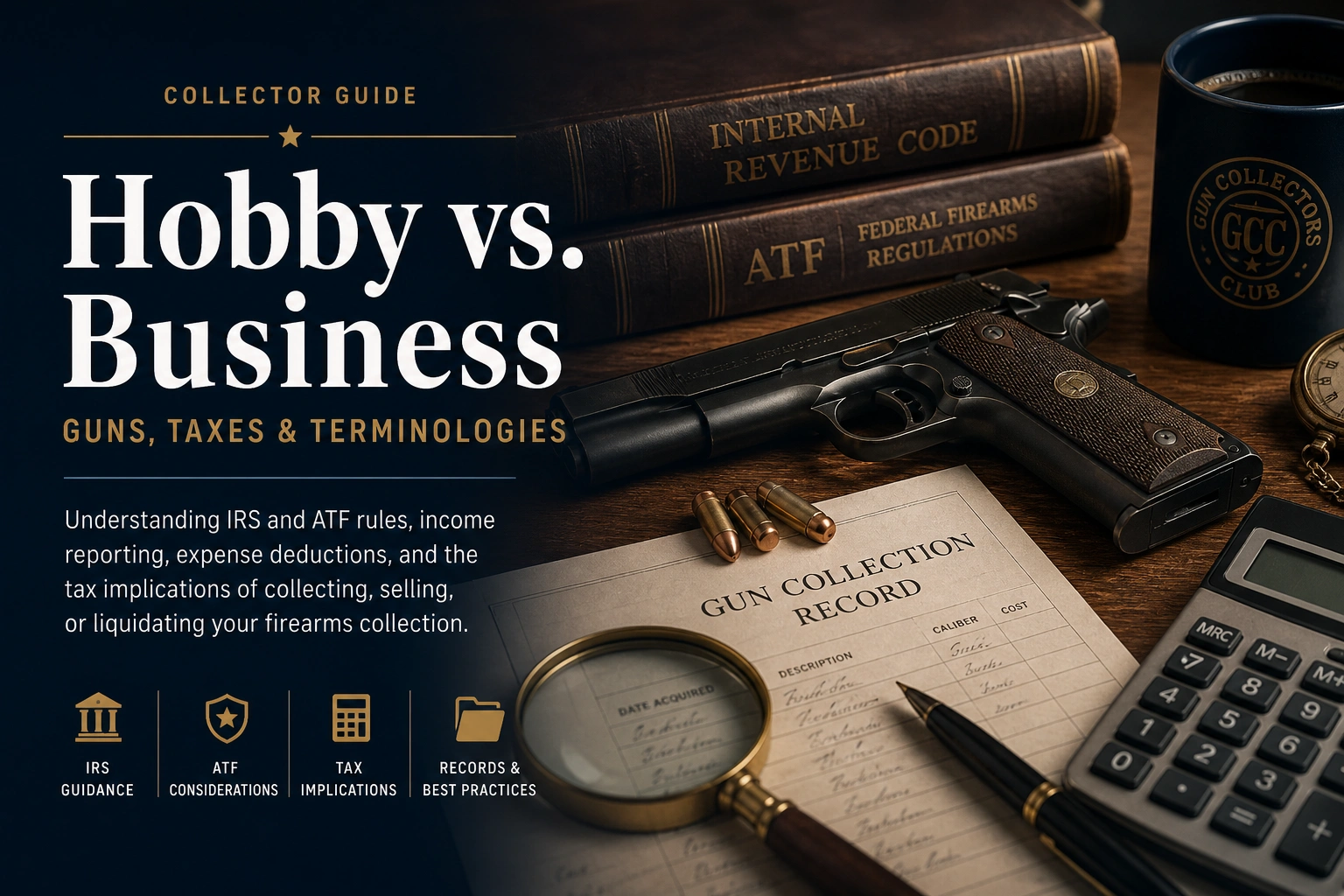

Guns, Taxes & Terminologies

This page is now positioned as a collector guide rather than a loose blog post. The point is practical: a gun collection may begin as a hobby, but records, sales, liquidation, and tax terminology can matter later for the collector, spouse, heirs, or tax advisor.

Important: this article is general commentary, not tax or legal advice. Firearms laws and tax treatment depend on the facts, timing, and jurisdiction.

A gun collection may eventually reach the point where liquidation becomes necessary. When that time comes, the considerations in Time to Downsize become highly relevant, especially for collectors transitioning from acquisition to disposition.

The IRS says ... Whether it’s something you’ve been doing for years, or something you just started in order to make extra money, taxpayers should report income earned from hobbies on their tax return.

The ATF says ... A Collectors License (C&R) does not authorize the collector to engage in the business of dealing in curios or relics. A dealer’s license must be obtained to engage in the business of dealing in any firearms, including curios or relics1.

USC 921 addresses the fact that you cannot be a "dealer in firearms" without a Federal Firearms License (FFL). (C) as applied to a dealer in firearms, as defined in section 921(a)(11)(A), a person who devotes time, attention, and labor to dealing in firearms as a regular course of trade or business with the principal objective of livelihood and profit through the repetitive purchase and resale of firearms, but such term shall not include a person who makes occasional sales, exchanges, or purchases of firearms for the enhancement of a personal collection or for a hobby, or who sells all or part of his personal collection of firearms.

And (22) The term "with the principal objective of livelihood and profit" means that the intent underlying the sale or disposition of firearms is predominantly one of obtaining livelihood and pecuniary gain, as opposed to other intents, such as improving or liquidating a personal firearms collection.

A business operates to make a profit. People engage in a hobby for sport or recreation, not to make a profit. But the lines can blur easily. There have been a lot of people that turned their hobby into a successful business. So how do you know when you cross that line?

Why does it matter if I classify my income as being from a hobby or a business? First, income from a hobby is reported on line 8, Schedule 1 of Form 1040 as miscellaneous income not subject to self-employment tax (Social Security and Medicare Tax) and you cannot deduct a loss from a hobby. If you report the income on Scedule C as a business, the net profit is subject to self-employment tax in addition to income tax.

Secondly, if you report income from your hobby, you cannot deduct expenses related to the production of that income (except the cost of the goods sold)2. Alternatively, if you report the income as a business on Schedule C, you can deduct all of your expenses that are considered reasonable, necessary or ordinary for the production of that income. You may even show a loss if the expenses exceed the income.

The fact is, since TCJA2, having a profitable hobby just got more expensive. I often say, if you look close enough, most things in life have a good side and a bad side and that is certainly true with the Tax Cuts & Jobs Act.

#1- I buy a gun for $1,000 and sell it for $2,000. My income is $1,000. I should report and pay income tax only on $1,000. I might put it on Line 8, Schedule 1 with a description of simply "Hobby Income." The Treasury or IRS has no requirement that I identify the source or even the type of hobby on the return. Just type of income, which is hobby, and amount, which is $1,000.

Since TCJA, I can no longer deduct my other expenses associated with this hobby income. Before, you could deduct hobby expenses (to the extent of income) as a Misc. Deduction Subject to 2% of AGI on Schedule A. That section of Schedule A has been deleted. For example, if I paid $200 advertising the gun for sale, no deduction. However, if the Auction House takes their $200 consignment fee before I get a check for the net amount, then my sales price is only $1,800. They pay the advertising and they can deduct it.

#2- I buy a gun for $3,600, later learn that it has been refinished from blue to nickle and sell it with disclosure for $2,000. I do not report the transaction on my income tax return at all. This is the same as before TCJA.

#1- I buy a gun for $1,000 and sell it for $2,000. My gross profit is $1,000. But I also deduct business expenses such as mileage to the gun store, gun shows, a trip to the indoor range and bank of $57. I also deduct subscription expense of $15 to a gun forum, bank charges for my separate business account of $60 and indoor range fees of $45 to test the gun.

After deducting my other expenses of $177 from my gross profit of $1,000, my net profit is $823 but I pay self-employment tax in addition to the income tax on that profit.

#2- I include the $2,000 revenue from the sale of the altered gun and include the cost of $3,600 in my Cost of Goods Sold (COGS) expense, $100 Other Expense for the cost of the Colt Archive Letter confirming the alteration and report a loss of ($1,700).

Once a gun collector ceases buying guns and begins liquidating them, clearly it is no longer a hobby.

Whether it takes one year or five to partially or wholly liquidate, for that period of time one might want to take the position that it is a business for income tax purposes. During this phase, documentation and provenance matter — topics explored in depth in the TAR‑40 Series and the K‑22 Masterpiece Series. You most assuredly will incur significant expenses in the liquidation process.

Frankly, for income tax purposes the door seems to be open to take the position that the income was derived from a hobby or that the income was derived from a business, depending on all of the facts and circumstances. That door is a swinging door. You might want to call it hobby income and under audit, the IRS might want to reclassify it as self-employment income subject to self-employment taxes (a business).

Some of you guys will want to hear this. The best evidence that you have not abandoned gun collecting as a hobby is to continue buying guns.

During the liquidation process you must follow all rules, regulations and laws concerning the transfer of ownership of a firearm. When the time comes, I can legally sell all of my guns from the collection, whether I have 40 or 400 without being classified as a firearms dealer as long as I do it properly. Personally I would not want a collection that large, but I have a friend that has more than 400 in his collection. It may take more than five years to liquidate that number successfully realizing the best prices.

One cannot argue that an activity cannot be a business because it would be illegal. Remember Al Capone? If Capone had only filed a Schedule C with a Business Code of 999999 Unable to Classify, reported his income and paid his taxes.

If the liquidation phase year(s) were reported on Schedule C with a personal tax return as a Sole Proprietor, the description of the business might be listed as Gun Collector with Business Code 453998, which is the NAICS Number for Collectors' Items. This code applies to certain store retailers and individual collectors even though they don't have a storefront.

Finally, if you collect antique firearms, ignore everything I've said so far and continue reading. The Flat 28% Collectibles Capital Gains Tax likely applies to you, unless your activity is a business.

This may be the only "antique" firearm you will see on these web pages. I don't own any antique firearms. Take note, it will be important later as you continue reading.

Although this gun is 98 years old, that's right, it will be 100 years old in 2022, it is not an antique! And in two years when it turns 100 years old, it still won't be an antique.

That's because they think in different terms. For example, in most states an automobile only has to be 25 to 35 years old to be classified as an antique for registration purposes. To the ATF this gun is a Curio & Relic (they have their own language). To the IRS it's just an asset or inventory item, but it is specifically not a collectible by their definition.

Gun Collectors have their own language as well and most tend to categorize guns into three categories or classes, a gun is either a "collector", a "shooter" or a "wall hanger." For more examples of how collectors distinguish these categories, see the Gun Library. A wall-hanger is a gun that cannot be safely fired and due to lack of value, rarity or condition does not meet collector status enough to warrant space in the display cabinet, undeserving, it is relegated to a conversation piece or used for decorative purposes. Generally speaking a shooter is a gun that is not quite collector grade, can be fired safely and without adversely affecting the value. To most, this gun is a shooter and in fact that is what I do with it, I shoot it.

Should you sell that gun you purchased back in 2016 in 2020 at a profit and report it on your income tax return, the IRS or a State Department of Revenue would have until April 15, 2024 to question or audit the transaction. That represents the three-year statute of limitations from the due date of the tax return for the 2020 tax year, April 15th, 2021 (or the date you filed, if later).

A very interesting email arrived in my inbox as I was preparing to write this article. The subject of the email message read ATF FFL ALERT - Federal Firearms Licensee Seminar August 2022.

The seminar will be held on Wednesday, August 31, 09:30 a.m. to 1 p.m., in the Priceville Town Hall, located at 242 Marco Drive, Decatur, AL 35603. You and your employees are invited and encouraged to attend the seminar. This seminar is for licensees, their employees, and authorized representatives only. This event is not open to the public.

Here are nine things the IRS says a Gun Collector should consider when determining if an activity such as liquidating a gun collection is a hobby or a business:

- Whether the activity is carried out in a business-like manner and the taxpayer maintains complete and accurate books and records.

- Whether the time and effort the taxpayer puts into the activity show they intend to make it profitable.

- Whether they depend on income from the activity for their livelihood.

- Whether any losses are due to circumstances beyond the taxpayer’s control or are normal for the startup phase of their type of business.

- Whether they change methods of operation to improve profitability.

- Whether the taxpayer and their advisors have the knowledge needed to carry out the activity as a successful business.

- Whether the taxpayer was successful in making a profit in similar activities in the past.

- Whether the activity makes a profit in some years and how much profit it makes.

- Whether the taxpayers can expect to make a future profit from the appreciation of the assets used in the activity.

All of these points are considerations you might want to discuss with a tax professional if you think your hobby might be turning into a business. My previous example of selling one gun may be over-simplified and of course you likely don't have a business if you are selling only one gun per year. But if you are selling one or two guns per month or consigning a dozen guns at a time to an auction house, maybe it is a business.

And naturally, the more activity you have, the more expenses you will have. For example, you may use your internet service and cell phone 50% for business use. I failed to include the cost of the ammunition used at the range to test the gun. And you might be depreciating assets used in the endeavor such as a gun safe, gun cabinet, desk and computer.

If you have no exit-strategy plan for your collection, these records could be worth their weight in gold to your family members or heirs. In my opinion, keeping good records are more important to the collector with no plan to sell off any of his or her collection.

At a minimum, the collector should maintain a listing of his guns with the make, model, serial number, cost and a good description that includes features and condition. This could be important for insurance purposes. Photos are good and should be stored in a location separate from the gun itself.

In addition to the basic information, I try to document as much history as possible, such as when, where, from whom and what I paid when I purchased the gun. If the seller provided any verbal info on the history of the gun, I make a note of it. Every Colt has a Colt Archive Letter. I also routinely update my records to reflect what I believe the current fair market value to be.

Under current tax law, knowing your cost basis in a gun might be important to your spouse, guardian or power of attorney in the event you were incapicitated and that person sold one or more of your guns. For example, if a gun sold at a profit, that person might be supposed to report the income on your tax return. If a gun sold at a loss, they would not have to report it on a tax return at all. But how would they know without a good record?

In the event of the death of a collector, his or her estate or heir would receive a "stepped-up" basis in the firearm to the fair market value (FMV) of the gun at the owner's date of death. No gain or loss would be recognized on the disposition for income tax purposes. And generally, if the gun is sold to an unrelated party within one year of your death, the sales price is considered to be the FMV. Selling within one year avoids the expense of having the collection appraised.

Many tax professionals inadvertantly report the sale of a gun as a capital gain subject to the 28% Collectibles Capital Gains Tax. Why does this happen? It is an uncommon occurrence for the tax preparer and rules regarding collectibles are very complex. And they take your word for it when you tell them you sold a collectible! Because the Gun Collector tells them he sold a collectible gun and a light goes on in their head. But the truth is, this is generally only true if the gun is an antique.

For the purposes of the National Firearms Act, the term “Antique Firearms†means any firearm not intended or redesigned for using rim fire or conventional center fire ignition with fixed ammunition and manufactured in or before 1898 (including any matchlock, flintlock, percussion cap or similar type of ignition system or replica thereof, whether actually manufactured before or after the year 1898) and also any firearm using fixed ammunition manufactured in or before 1898, for which ammunition is no longer manufactured in the United States and is not readily available in the ordinary channels of commercial trade.

There are four tax brackets that are lower than the 28% flat Collectibles Capital Gains Tax rate: 10%, 12%, 22% and 24%. So if you properly tell your tax guy that you have hobby income, it triggers a different light to go on in their head and you may pay less, which would be the correct amount of tax.

But, the IRS has the authority to deem any tangible property not specifically listed, as a collectible and they have. For example, restored automobiles, valuable baseball cards and even rare comic books just to name a few.

It would be improper and a mistake for the Gun Collector to arbitrarily deem, label or classify any sale of a non-antique gun as a Collectible Capital Gain instead of Hobby Income for tax purposes. Now you may want it to be, if you are in the 32%, 35% or 37% tax brackets. Whichever side of the argument you may be on, the only way your non-antique gun should be classified as a collectible for tax purposes by the IRS is if it is extremely rare, maybe. See what I wrote on the Colt Python.

For you gun lovers, the following is known as "situational awareness." You may not want to think about any of this now. You may not even want to know about some of this. But some of this information could be important to you or your family down the road. And it's always best not to be blind-sided.

If your cost basis in the collection is $50,000 and the fair market value of the collection is $150,000, the $100,000 of income could have significant tax consequences. Depending on your personal set of facts and circumstances, it could for example cause you to pay income taxes on up to 85% of the Social Security Benefits you and your wife are drawing. And to boot, Medicare might raise your premiums to the maximum $4,000 each for one year until your income comes back down in the following tax year.

Proper tax planning with a tax professional such as an Enrolled Agent, CPA or Attorney that specializes in tax can answer whether this would be good or bad for you tax-wise. I have seen cases where having $33,333 extra income per year for three years can be better or WORSE than having $100,000 extra income in one tax year. Don't assume staying in a lower tax bracket is always better.

The best example is when a taxpayer is not normally paying income tax on Social Security Benefits, but the extra income pushes them over the threshold. So although spreading over three years the $33,333 of extra income keeps you in the 22% tax bracket, if it causes you to pay 22% on $33,333 of SS benefits, that's the same as paying 44% on the extra income for three years. Whereas having the entire $100,000 extra income in one tax year may cause you to pay at the next higher bracket of 24% on some of the monies, it only hits the SS benefits one time instead of three.

The advantage is the step-up in basis that the heir receives. In my example, the $50,000 cost basis gets stepped-up to $150,000 FMV and no income tax is due at all if the collection is sold within one year of the date of death4. If the collection is held longer than one year after date of death (DOD), there may be some appreciation after the DOD to take into account. Discussing this with your wife, children or heirs in advance is a good idea.

A widow lady came to see me shortly after her husband died and confided that she was having trouble sleeping with all of those guns in the house and him not there. She and her husband had discussed the guns before, but as she trembled, she told me at that time she had no idea that she would feel this way. Her fear was that men would come and break-in at night to steal them while she's there alone.

If you gift a gun to Nephew George during your lifetime, his cost basis in the gun becomes whatever your cost basis was in the gun. As long as the current fair market value of the gift is less than $15,000 (the annual gifting exclusion amount to any one person) no Gift Tax Return is required. Neither you or George have to report anything on your income tax returns. George will not pay income tax on the gift and you cannot take a deduction on your taxes for the gift. Nephew George is likely not a registered charity.

But, there is almost always a "but." Should you die within two years of making the gift, Nephew George may be entitled to a stepped-up basis to FMV (or the gift may stand). That is because under the tax code, the gift would be deemed to have been made in "contemplation of death", whether you were actually contemplating death or not. That was the good news! The bad news is that your Executor would have to include the FMV of the gift in your Taxable Estate if your estate exceeds $11.58 million.

There may be legal ramifications. Are you positive Nephew George can legally own a firearm? I might take the gun to the local gun store and let Nephew George go do the paperwork and pick it up there. My local gun store guy said they would only charge a $30 transfer fee to do the background check and log the paperwork.

Under Age 65 - If you are under age 65 drawing early or reduced benefits and classifying the income as hobby income, no. Hobby income is not subject to self-employment tax and therefor not considered "earned income" for this purpose. If you report the income as business income, yes if the income exceeds certain thresholds. You may have to repay $1 of benefits for every $2 earned.

Age 65 or Over - If you are age 65 or over you can have an unlimited amount of income from a business or hobby and not have to repay any benefits. Either case however, may cause you to have to pay income tax on up to 85% of those benefits.

Terms can have very different meanings to different people, groups or organizations. I hope you see that terminology used by Gun Collectors, Non-Collectors, the ATF and the IRS may not share the same meaning in particular technical applications.

Occassionally, even people within what might be considered an industry use terms differently, take some gun dealers for example. How many times have you seen a gun advertised for sale with hyperbole like this in the desciption? Highly Collectible! Extremely Rare! To whom? Just because that old Colt Python is the only one he's taken in as a trade-in the last 15 years may make it rare to him. But there are three-quarters of a million of them floating around out there.

And what about that gun that has been refinished, had the grips replaced, the sights modified and maybe even been scratched up by someone who should not be engraving a gun at all? Perhaps it is still collectible to some, but certainly not all. Even a 1932 Ford can lose its classification as an antique once it is highly modified to be a hot-rod, street-rod or race-car.

Time to DownsizeRecordkeeping Tools & Bench Gear

Collectors should keep purchase records, sales records, serial numbers, archive letters, photographs, and condition notes. I keep a curated gear list for tools, books, storage, and recordkeeping items that fit the way I work.

Browse My Gear ListAs an Amazon Associate I earn from qualifying purchases. I only link to products, books, tools, and accessories that fit the editorial purpose of Gun Collectors Club.

About Greg Cook

Greg Cook writes about firearms collecting, personal history, and the stories behind interesting guns. His Army MOS was 76Y, Unit Armorer, and he brings that practical background to his collector articles.

Note1 - Source: https://www.atf.gov/rules-and-regulations/final-rule-definition-engaged-business-a-dealer-firearms

Note2 - Prior to the Tax Cuts and Jobs Act (TCJA) you could deduct hobby expenses associated with hobby income, up to the amount of income you were reporting from the hobby, as an itemized deduction if the expenses exceeded 2% of your adjusted gross income. No more.

Note3 - The types of assets that are collectibles are listed in IRC Sec. 408(m) and proposed regulations. Proposed Regulation Sec. 1.408-10(b)5 expands the Sec. 408(m)(2) definition of a collectible to also include: Any musical instrument; and Any historical objects (documents, clothes, etc.).

Note4 - If you live in a Community Property State, your surviving spouse may be entitled only to a one-half step-up in basis at your death, ie, as in the example one-half of $50,000 original cost basis equals $25,000 plus one-half of FMV at DOD of $75,000 equals adjusted basis of $100,000 in your surviving spouse's hands.

Disclaimer: Nothing in this article should be considered tax or legal advice. Consult your tax advisor about your specific facts and circumstances. And importantly, there are considerations other than income tax when it comes to converting a hobby to a business, business license for example and potentially sales tax, both of which would generally be the responsibility of your consignment intermediary whether it be an auction house or dealer.

The Footnotes and Disclaimer are an integral part of this blog article. If you print this article, they must be retained with it.